Germany – Full Blown Recession or Summer Slump?

By Alison Schonberg, 10/24/14

Germany is the Eurozone’s economic lynchpin. During the Eurozone Crisis, Angela Merkel and her political bloc encouraged strict austerity measures, like budget slashing and deficit reduction, and discouraged calls for expansionary policy. In spite of opposition from France, Italy, Spain, and other poor-performing members of the currency union, Germany continued to dominate economic policy. So long as the country boasted strong industrial production, foreign investment, and merchandise trade, it could justify policy leadership, and harsh intervention.

Now, in light of weak economic projections, and a prospective recession, Germany’s leadership has suddenly come into question. Should Germany continue as policy leader, or allow countries like France and Italy more power and flexibility? Are austerity measures really the best way to combat recession, or should Germany and the Eurozone consider alternatives? Is Germany really headed for recession, or just a temporary slump?

A Look at Expectations:

Economic policymakers who anticipate a German recession typically cite three indicators: 1) the country’s merchandise trade position, 2) investment climate, and 3) industrial production.

Let’s take a quick look at each measure of economic performance, and see if they really point toward a recession. First – Germany’s trade position. Looking at August data, German merchandise exports fell 5.8%, imports 1.3%. Now, in order to determine whether or not these values are significant, we have to look at them in context. Namely, what is Germany’s trade-to-GDP ratio? In the United States, where trade accounts for only 23.9% of GDP, a 5% decrease would be problematic, but not the end of the world. In Germany, where combined merchandise imports and exports account for a whopping 75.1% of GDP, the drop is much more ominous. If German exports continue to drop, they could have a strong negative impact on GDP estimates. More importantly, though, falling German exports also indicate low demand in the Eurozone. As of 2012, Germany was both the third largest exporter, and the third largest importer, with France, the UK, the Netherlands, and China as its most significant trading partners. German exports are falling for two reasons: declining performance among developing countries, but mostly nonexistent demand among its Eurozone partners. The more Germany insists on contractionary policy (especially in France), the more it risks damaging its own export demand. Under austerity policies, French price levels, wages, and overall demand decreases, the country buys fewer imports, and German exports decline. In this way, German policy both stifles its trading partners, and inhibits domestic growth. If Germany allowed expansionary policy, however, both Germany and its Eurozone neighbors could grow – trading partners could experience higher levels of employment and wage growth, while Germany could experience higher demand for its exports.

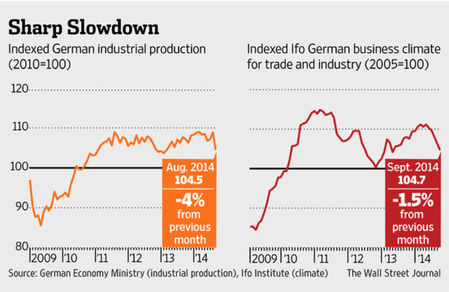

Clearly, trade data points to a German recession – a vicious cycle of declining export demand. Now, let’s shift to investment climate and industrial production. Both indicators look weak, but do not carry the same long-term implications. When we consider both values in context, we should evaluate them on two criteria: their long-term impact, and to what extent they influence Eurozone growth. Addressing the first question, it seems unclear whether downturns are temporary or not. In August, the indexed measure of German Business Climate for Trade and Business was down 1.5% from the previous month, and German Industrial Production down 4% from the previous month. First, looking at investment climate, the data appears long-term. Germany’s investment climate index is at its “lowest level since January 2013”, and continues to decline, but its Eurozone impact is limited. German businesses are reluctant to invest in domestic projects, so they hamper German rather than Eurozone growth. When we evaluate industrial production, we draw similar conclusions; data from August is significant in a domestic context, and could certainly contribute to low GDP estimates, but does not have a strong global effect. A 4% decrease in industrial production certainly stands out. When we look at the previous four months: 1.9% increase in July, 0.3% increase in June, and a 1.8% decrease in May, 4% is a drastic, sudden decrease. The indicator highlights the same domestic problem, however: weak confidence among German investors, and reduced spending in German industry.

Conclusions and Ramifications for Policy:

Based on our analysis above, it seems that Germany is more than likely headed for a recession, or at least will drag on Eurozone growth. Germany’s policy response is much more uncertain, though. When asked about weak investment, production, and export numbers, President Angela Merkel insists causes are either temporary, or beyond her control. In particular, she blames adjusted vacation times – moved from July to August – and an ongoing crisis in Ukraine, as justifications for weak domestic performance. She insists these indicators will not impact Eurozone growth, though, and can only improve with time.

While a change of policy is unlikely, given President Merkel’s outlook, Germany might need new policies. Fortunately, there are two pretty manageable alternatives at its disposal: 1) abandon austerity policy, and pursue expansionary instead, or 2) adopt something similar to the Federal Reserve’s “Operation Twist,” and indirectly target interest rates through the yield curve. Both could easily correct for a month or two of weak growth, but are unlikely solutions. If Germany altered its policy, officials would have to reconsider their positions toward France, Italy and other austerity opponents. Germany would set a dangerous precedent for other Eurozone countries already clamoring for expansionary policy. Countries like France and Italy would suddenly have an excuse to resume out of control spending, and raise already high debt to GDP ratios. For this reason, Germany is much more likely wait out a crisis, and stick stubbornly to its austerity policies.

A note – most of the data that appears in this blog post reflects August data, released during September 2014.

Germany is the Eurozone’s economic lynchpin. During the Eurozone Crisis, Angela Merkel and her political bloc encouraged strict austerity measures, like budget slashing and deficit reduction, and discouraged calls for expansionary policy. In spite of opposition from France, Italy, Spain, and other poor-performing members of the currency union, Germany continued to dominate economic policy. So long as the country boasted strong industrial production, foreign investment, and merchandise trade, it could justify policy leadership, and harsh intervention.

Now, in light of weak economic projections, and a prospective recession, Germany’s leadership has suddenly come into question. Should Germany continue as policy leader, or allow countries like France and Italy more power and flexibility? Are austerity measures really the best way to combat recession, or should Germany and the Eurozone consider alternatives? Is Germany really headed for recession, or just a temporary slump?

A Look at Expectations:

Economic policymakers who anticipate a German recession typically cite three indicators: 1) the country’s merchandise trade position, 2) investment climate, and 3) industrial production.

Let’s take a quick look at each measure of economic performance, and see if they really point toward a recession. First – Germany’s trade position. Looking at August data, German merchandise exports fell 5.8%, imports 1.3%. Now, in order to determine whether or not these values are significant, we have to look at them in context. Namely, what is Germany’s trade-to-GDP ratio? In the United States, where trade accounts for only 23.9% of GDP, a 5% decrease would be problematic, but not the end of the world. In Germany, where combined merchandise imports and exports account for a whopping 75.1% of GDP, the drop is much more ominous. If German exports continue to drop, they could have a strong negative impact on GDP estimates. More importantly, though, falling German exports also indicate low demand in the Eurozone. As of 2012, Germany was both the third largest exporter, and the third largest importer, with France, the UK, the Netherlands, and China as its most significant trading partners. German exports are falling for two reasons: declining performance among developing countries, but mostly nonexistent demand among its Eurozone partners. The more Germany insists on contractionary policy (especially in France), the more it risks damaging its own export demand. Under austerity policies, French price levels, wages, and overall demand decreases, the country buys fewer imports, and German exports decline. In this way, German policy both stifles its trading partners, and inhibits domestic growth. If Germany allowed expansionary policy, however, both Germany and its Eurozone neighbors could grow – trading partners could experience higher levels of employment and wage growth, while Germany could experience higher demand for its exports.

Clearly, trade data points to a German recession – a vicious cycle of declining export demand. Now, let’s shift to investment climate and industrial production. Both indicators look weak, but do not carry the same long-term implications. When we consider both values in context, we should evaluate them on two criteria: their long-term impact, and to what extent they influence Eurozone growth. Addressing the first question, it seems unclear whether downturns are temporary or not. In August, the indexed measure of German Business Climate for Trade and Business was down 1.5% from the previous month, and German Industrial Production down 4% from the previous month. First, looking at investment climate, the data appears long-term. Germany’s investment climate index is at its “lowest level since January 2013”, and continues to decline, but its Eurozone impact is limited. German businesses are reluctant to invest in domestic projects, so they hamper German rather than Eurozone growth. When we evaluate industrial production, we draw similar conclusions; data from August is significant in a domestic context, and could certainly contribute to low GDP estimates, but does not have a strong global effect. A 4% decrease in industrial production certainly stands out. When we look at the previous four months: 1.9% increase in July, 0.3% increase in June, and a 1.8% decrease in May, 4% is a drastic, sudden decrease. The indicator highlights the same domestic problem, however: weak confidence among German investors, and reduced spending in German industry.

Conclusions and Ramifications for Policy:

Based on our analysis above, it seems that Germany is more than likely headed for a recession, or at least will drag on Eurozone growth. Germany’s policy response is much more uncertain, though. When asked about weak investment, production, and export numbers, President Angela Merkel insists causes are either temporary, or beyond her control. In particular, she blames adjusted vacation times – moved from July to August – and an ongoing crisis in Ukraine, as justifications for weak domestic performance. She insists these indicators will not impact Eurozone growth, though, and can only improve with time.

While a change of policy is unlikely, given President Merkel’s outlook, Germany might need new policies. Fortunately, there are two pretty manageable alternatives at its disposal: 1) abandon austerity policy, and pursue expansionary instead, or 2) adopt something similar to the Federal Reserve’s “Operation Twist,” and indirectly target interest rates through the yield curve. Both could easily correct for a month or two of weak growth, but are unlikely solutions. If Germany altered its policy, officials would have to reconsider their positions toward France, Italy and other austerity opponents. Germany would set a dangerous precedent for other Eurozone countries already clamoring for expansionary policy. Countries like France and Italy would suddenly have an excuse to resume out of control spending, and raise already high debt to GDP ratios. For this reason, Germany is much more likely wait out a crisis, and stick stubbornly to its austerity policies.

A note – most of the data that appears in this blog post reflects August data, released during September 2014.