Oil-ogopoly to Monopoly – How Saudi Arabia Outlasts Rivals

By Alison Schonberg, 11/9/14

Topic overview:

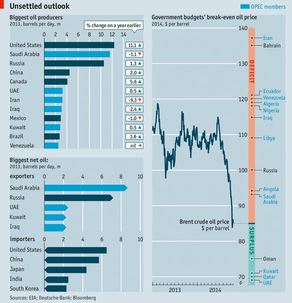

Since mid-October, oil prices have fallen from $115 to $85 per barrel. For now, economists are reluctant to call this a win or a loss for the global economy; dramatic price changes certainly benefit consumers, importers, and countries with energy-intensive agricultural industries, but could have disastrous effects on exporters. In particular, Iran, Venezuela, Russia, and Saudi Arabia are four countries that rely on exports to support expensive social projects, prop-up unpopular regimes, and compensate for high budget deficits. Among the three principal “losers,” though, there is a clear outlier – Saudi Arabia. In contrast to other large exporters, Saudi Arabia has the financial resources to not only survive, but potentially grow during a period of long-term price decline. What makes the Arab kingdom different, though? How can an oil exporter come out on top, when its biggest asset is dropping in value?

#1 Survival Tool: Foreign Reserves:

While reading about oil prices, I found many similarities between exporters – high market share, state-control of the energy sector, and total dependence on exports. One factor distinguishes Saudi Arabia, though - foreign reserves. They are one of the most powerful, versatile tools in a central bank’s arsenal, and can help during periods of export decline, inflation, currency speculation, and potential default. Foreign reserves include those international currencies kept in the central bank, which officials can sell or buy to manipulate exchange rates, and balance budgets.

Looking specifically at the current oil crisis, countries with huge foreign reserves are at a clear advantage for two reasons: 1) government officials can dip into accumulated reserves to avoid excessive deficit values, and 2) central bankers can maintain international competitiveness by adjusting the value of their currency, and fending off speculative attacks.

Managing Budget Deficits:

When oil prices decrease, state-owned energy companies experience a dip in revenue. For example, Saudi Arabia, which relies on oil profits for 90% of federal funding, has difficulty managing expenses. With oil at a lower price, and timid demand from major importers like China, state projects become unsustainable. Those countries with limited foreign reserves have two options: slash their budgets, or default. Those with foreign reserves, however, have a loophole, and can manage in the short-term, selling off US Treasuries to finance large budget deficits. While other countries cannot afford to pay off deficits between 1-2% of annual GDP, Saudi Arabia is well equipped to manage its drop in profits. The country’s foreign exchange reserves amount to $768.5 billion dollars, denominated in one of the world’s safest bills – US Treasuries. In context, only two other countries boast greater reserves: China, which uses US dollars to preserve an artificially low exchange rate, and Japan, which also uses dollars for policy intervention.

By contrast, Iran, Russia, and Venezuela have comparatively weaker resources. In a list of countries by foreign exchange reserves, their respective rankings were 32, 6, and 58. One could argue that Russia is in a better position than Iran and Venezuela, given its higher ranking, but it is nowhere near as strong as Saudi Arabia, with an estimated difference in reserves up to $314 billion. In other words, when Saudi Arabian revenue decreases, they can handle a much larger gap between oil profits and government spending.

Stabilizing Exchange Rates:

Another way Saudi Arabia can use its foreign reserves, and outlast oil-producing competitors, is through currency manipulation. When the price of a country’s largest export drops, and isn’t followed by an increase in demand, net exports fall. Exports and imports are significant components of current account: (exports-imports) + net income from abroad + net unilateral transfers from abroad. When current account decreases, a country’s currency depreciates in value, and domestic goods become cheaper relative to foreign goods. Now, the country’s central bank can either welcome the depreciation, and hope it stimulates greater exports, or sterilize the change in exchange rate. For many oil producers with weak foreign investment, or fixed exchange rates, depreciation can trigger a currency crisis.

In Saudi Arabia’s case, the riyal is pegged to the US dollar, so the central bank must compensate for depreciation by selling foreign reserves, decreasing the money supply, and returning to exchange-rate equilibrium. Some oil competitors, like Venezuela, are more likely to experience a crisis. With few foreign reserves, the central bank will not be able to address depreciation, or maintain its pegged bolívar.

Now, what about Russia and Iran? Neither state has a fixed exchange rate, but both have a vested interest in maintaining strong, stable exchange rates. If either country’s currency depreciates, it will pay more for imports, and lose valuable foreign investment. Considering that both are subject to international sanctions, foreign direct investment is already vulnerable. Currency depreciation, with no foreign reserves to counteract the change in exchange rate, can leave both countries weak, starved for investment, and unable to afford valuable imports.

Conclusion: Is Saudi Arabia Really Safe?

Saudi Arabia is likely to survive the current downturn in oil prices, provided that demand picks up within the next year. The oil giant does face a few risks, though. Whenever a country relies too much on foreign reserves, its greatest danger is a speculative attack. If international investors begin to doubt Saudi Arabia, see few changes in its government spending, or wonder if the Saudi government can cover huge deficits, then a few might buy back foreign reserves. When a few investors remove their reserves, others will likely follow, trapped in a panic spiral. If this occurs, investors could remove Saudi Arabia’s reserve cushion; the country would face unmanageable deficits, and in the worst-case scenario, default.

This scenario is unlikely though. As of 2013, Saudi Arabia was the “largest recipient of foreign direct investment in the Gulf and the Middle East,” so as long as investors remain confident, and Saudi Arabia makes some effort to limit public spending, then it could survive this period of falling oil prices.

Topic overview:

Since mid-October, oil prices have fallen from $115 to $85 per barrel. For now, economists are reluctant to call this a win or a loss for the global economy; dramatic price changes certainly benefit consumers, importers, and countries with energy-intensive agricultural industries, but could have disastrous effects on exporters. In particular, Iran, Venezuela, Russia, and Saudi Arabia are four countries that rely on exports to support expensive social projects, prop-up unpopular regimes, and compensate for high budget deficits. Among the three principal “losers,” though, there is a clear outlier – Saudi Arabia. In contrast to other large exporters, Saudi Arabia has the financial resources to not only survive, but potentially grow during a period of long-term price decline. What makes the Arab kingdom different, though? How can an oil exporter come out on top, when its biggest asset is dropping in value?

#1 Survival Tool: Foreign Reserves:

While reading about oil prices, I found many similarities between exporters – high market share, state-control of the energy sector, and total dependence on exports. One factor distinguishes Saudi Arabia, though - foreign reserves. They are one of the most powerful, versatile tools in a central bank’s arsenal, and can help during periods of export decline, inflation, currency speculation, and potential default. Foreign reserves include those international currencies kept in the central bank, which officials can sell or buy to manipulate exchange rates, and balance budgets.

Looking specifically at the current oil crisis, countries with huge foreign reserves are at a clear advantage for two reasons: 1) government officials can dip into accumulated reserves to avoid excessive deficit values, and 2) central bankers can maintain international competitiveness by adjusting the value of their currency, and fending off speculative attacks.

Managing Budget Deficits:

When oil prices decrease, state-owned energy companies experience a dip in revenue. For example, Saudi Arabia, which relies on oil profits for 90% of federal funding, has difficulty managing expenses. With oil at a lower price, and timid demand from major importers like China, state projects become unsustainable. Those countries with limited foreign reserves have two options: slash their budgets, or default. Those with foreign reserves, however, have a loophole, and can manage in the short-term, selling off US Treasuries to finance large budget deficits. While other countries cannot afford to pay off deficits between 1-2% of annual GDP, Saudi Arabia is well equipped to manage its drop in profits. The country’s foreign exchange reserves amount to $768.5 billion dollars, denominated in one of the world’s safest bills – US Treasuries. In context, only two other countries boast greater reserves: China, which uses US dollars to preserve an artificially low exchange rate, and Japan, which also uses dollars for policy intervention.

By contrast, Iran, Russia, and Venezuela have comparatively weaker resources. In a list of countries by foreign exchange reserves, their respective rankings were 32, 6, and 58. One could argue that Russia is in a better position than Iran and Venezuela, given its higher ranking, but it is nowhere near as strong as Saudi Arabia, with an estimated difference in reserves up to $314 billion. In other words, when Saudi Arabian revenue decreases, they can handle a much larger gap between oil profits and government spending.

Stabilizing Exchange Rates:

Another way Saudi Arabia can use its foreign reserves, and outlast oil-producing competitors, is through currency manipulation. When the price of a country’s largest export drops, and isn’t followed by an increase in demand, net exports fall. Exports and imports are significant components of current account: (exports-imports) + net income from abroad + net unilateral transfers from abroad. When current account decreases, a country’s currency depreciates in value, and domestic goods become cheaper relative to foreign goods. Now, the country’s central bank can either welcome the depreciation, and hope it stimulates greater exports, or sterilize the change in exchange rate. For many oil producers with weak foreign investment, or fixed exchange rates, depreciation can trigger a currency crisis.

In Saudi Arabia’s case, the riyal is pegged to the US dollar, so the central bank must compensate for depreciation by selling foreign reserves, decreasing the money supply, and returning to exchange-rate equilibrium. Some oil competitors, like Venezuela, are more likely to experience a crisis. With few foreign reserves, the central bank will not be able to address depreciation, or maintain its pegged bolívar.

Now, what about Russia and Iran? Neither state has a fixed exchange rate, but both have a vested interest in maintaining strong, stable exchange rates. If either country’s currency depreciates, it will pay more for imports, and lose valuable foreign investment. Considering that both are subject to international sanctions, foreign direct investment is already vulnerable. Currency depreciation, with no foreign reserves to counteract the change in exchange rate, can leave both countries weak, starved for investment, and unable to afford valuable imports.

Conclusion: Is Saudi Arabia Really Safe?

Saudi Arabia is likely to survive the current downturn in oil prices, provided that demand picks up within the next year. The oil giant does face a few risks, though. Whenever a country relies too much on foreign reserves, its greatest danger is a speculative attack. If international investors begin to doubt Saudi Arabia, see few changes in its government spending, or wonder if the Saudi government can cover huge deficits, then a few might buy back foreign reserves. When a few investors remove their reserves, others will likely follow, trapped in a panic spiral. If this occurs, investors could remove Saudi Arabia’s reserve cushion; the country would face unmanageable deficits, and in the worst-case scenario, default.

This scenario is unlikely though. As of 2013, Saudi Arabia was the “largest recipient of foreign direct investment in the Gulf and the Middle East,” so as long as investors remain confident, and Saudi Arabia makes some effort to limit public spending, then it could survive this period of falling oil prices.