The Latest on Obamacare

By Matthew Hersman, 04/06/2014

With the last days of the Individual Marketplace winding down as Americans only have until March 31st to sign up for insurance, the final numbers of enrollees are coming in. While it becomes clearer that the government is likely to fall short of its goal of 7 million enrollees, the numbers are not as bad as opponents, who feared the “death spirals,” predicted they would be. As of March 17, the Department of Health and Human Services released the latest number of enrollees on the Marketplace to be 5 million, with some experts predicting the number to increase to 6 million by the time it closes. Obama explained the significance of these numbers when he said “the more you can spread the risk with more people, the better deal you are going to get.” Obamacare runs on the necessity that enough young, healthy people sign up in order to balance out the financial burden from the older Americans who tend to increase costs for the system. Therefore, due to the underperformance of the rollout and the less-than-expected number of young and healthy enrollees, reports show that insurance companies will likely react by increasing premiums, with some estimates pointing to a 20% to 40% increase in the year 2015. This shows that while the Affordable Care Act does appear to have received an adequate number of enrollees to continue, the lower-than-expected numbers will likely come at a cost in the future.

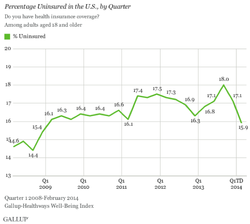

Nevertheless, the question of whether Obamacare truly “succeeded” in achieving its goals still remains. After all, the overarching goal was not to implement a renovated healthcare system just to see if we could, but rather was implemented in order to lower the rate of uninsured Americans. However, the problem with evaluating this issue is due to a simple reason, and that is because the new enrollees on the Insurance Marketplace were not asked about previous insurance coverage. This means that there is no concrete data on the exact number of Americans who are now signed up that were previously uninsured. However, not all hope is lost. The graph to the left indicates some promising signs, which shows a significant decrease in the amount of uninsured Americans, from 18% in the third quarter of 2013 down to 15.9% in the most recent estimates, the lowest they have been since 2008. Yet, a gloomier survey by McKinsey indicates that as low as only 14% of the new enrollees on the Marketplace were formerly uninsured, with the rest signing up either due to cheaper coverage compared to what their employers are offering them, switching plans due to cancellation of old plans, or because they were previously covered on the former individual market. While it will be difficult to definitively measure the exact number of Americans that gained insurance as a result of the Affordable Care Act, our best indicators at evaluating the new system will come when we receive the total number of uninsured Americans at the close of the market.

While it is likely that the Affordable Care Act did obtain enough enrollees to be sustainable, this does not mean that there are no improvements that can be made. For example, while many attribute their lack of health insurance due to it being “too expensive,” a large number of uninsured Americans may not have signed up due to simple misinformation. In a telephone survey run by Bankrate, when respondents were asked whether “tax credits are available through the Affordable Care Act to reduce the monthly price of health insurance,” only 30% were able to give a definitive “yes” as an answer. Deborah Chollet, a health insurance research leader at Mathematica Policy Research in Washington, D.C., attributes this lack of information to poor marketing. She states, "low-income, young families may have been overlooked. They're probably not spending a lot of time watching television, they never read a newspaper, and if they listen to radio, it's probably music in the car.” Stories like this indicate that a better job needs to be done in signing up more Americans. If the administration fails in doing so, premiums will continue to climb and dissuade further Americans from signing up.